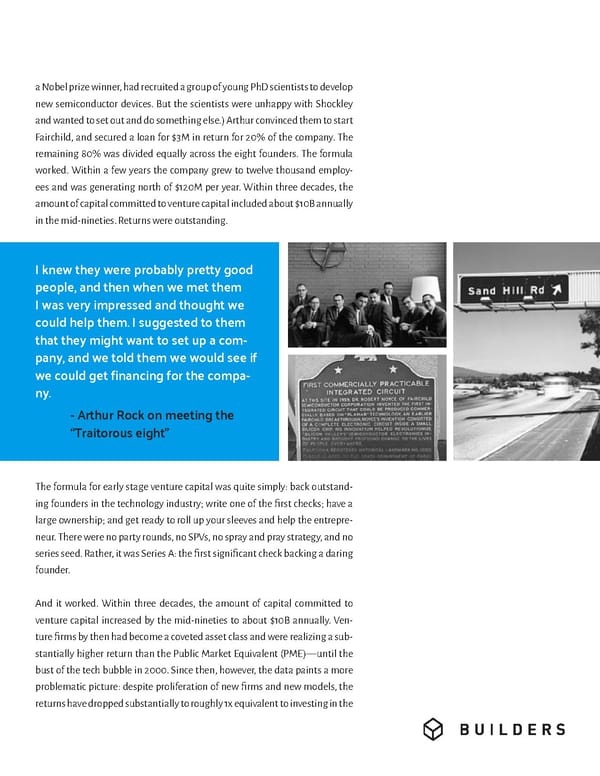

a Nobel prize winner, had recruited a group of young PhD scientists to develop new semiconductor devices. But the scientists were unhappy with Shockley and wanted to set out and do something else.) Arthur convinced them to start Fairchild, and secured a loan for $3M in return for 20% of the company. The remaining 80% was divided equally across the eight founders. The formula worked. Within a few years the company grew to twelve thousand employ- ees and was generating north of $120M per year. Within three decades, the amount of capital committed to venture capital included about $10B annually in the mid-nineties. Returns were outstanding. I knew they were probably pretty good people, and then when we met them I was very impressed and thought we could help them. I suggested to them that they might want to set up a com- pany, and we told them we would see if we could get financing for the compa- ny. - Arthur Rock on meeting the “Traitorous eight” The formula for early stage venture capital was quite simply: back outstand- ing founders in the technology industry; write one of the first checks; have a large ownership; and get ready to roll up your sleeves and help the entrepre- neur. There were no party rounds, no SPVs, no spray and pray strategy, and no series seed. Rather, it was Series A: the first significant check backing a daring founder. And it worked. Within three decades, the amount of capital committed to venture capital increased by the mid-nineties to about $10B annually. Ven- ture firms by then had become a coveted asset class and were realizing a sub- stantially higher return than the Public Market Equivalent (PME) — until the bust of the tech bubble in 2000. Since then, however, the data paints a more problematic picture: despite proliferation of new firms and new models, the returns have dropped substantially to roughly 1x equivalent to investing in the

Venture Capital - Back To Basics Page 2 Page 4

Venture Capital - Back To Basics Page 2 Page 4