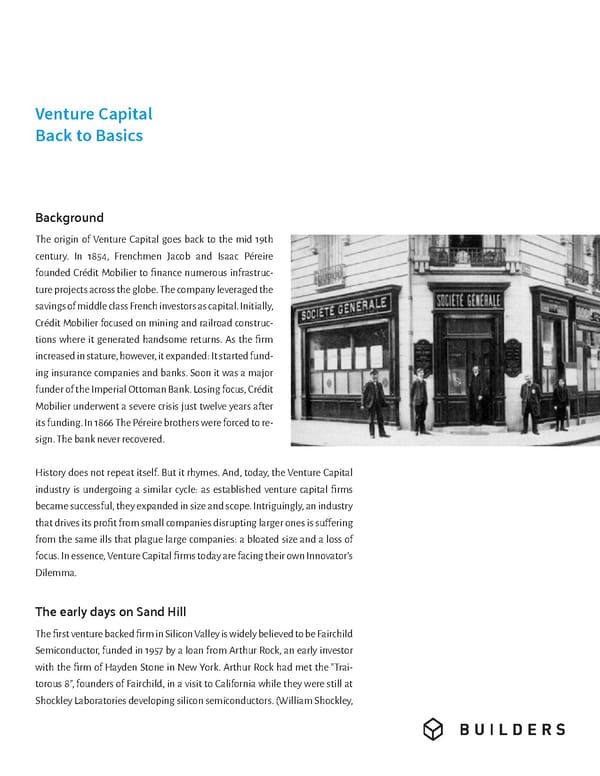

Venture Capital Back to Basics Background The origin of Venture Capital goes back to the mid 19th century. In 1854, Frenchmen Jacob and Isaac Péreire founded Crédit Mobilier to finance numerous infrastruc- ture projects across the globe. The company leveraged the savings of middle class French investors as capital. Initially, Crédit Mobilier focused on mining and railroad construc- tions where it generated handsome returns. As the firm increased in stature, however, it expanded: It started fund- ing insurance companies and banks. Soon it was a major funder of the Imperial Ottoman Bank. Losing focus, Crédit Mobilier underwent a severe crisis just twelve years after its funding. In 1866 The Péreire brothers were forced to re- sign. The bank never recovered. History does not repeat itself. But it rhymes. And, today, the Venture Capital industry is undergoing a similar cycle: as established venture capital firms became successful, they expanded in size and scope. Intriguingly, an industry that drives its profit from small companies disrupting larger ones is suffering from the same ills that plague large companies: a bloated size and a loss of focus. In essence, Venture Capital firms today are facing their own Innovator’s Dilemma. The early days on Sand Hill The first venture backed firm in Silicon Valley is widely believed to be Fairchild Semiconductor, funded in 1957 by a loan from Arthur Rock, an early investor with the firm of Hayden Stone in New York. Arthur Rock had met the “Trai- torous 8”, founders of Fairchild, in a visit to California while they were still at Shockley Laboratories developing silicon semiconductors. (William Shockley,

Venture Capital - Back To Basics Page 1 Page 3

Venture Capital - Back To Basics Page 1 Page 3