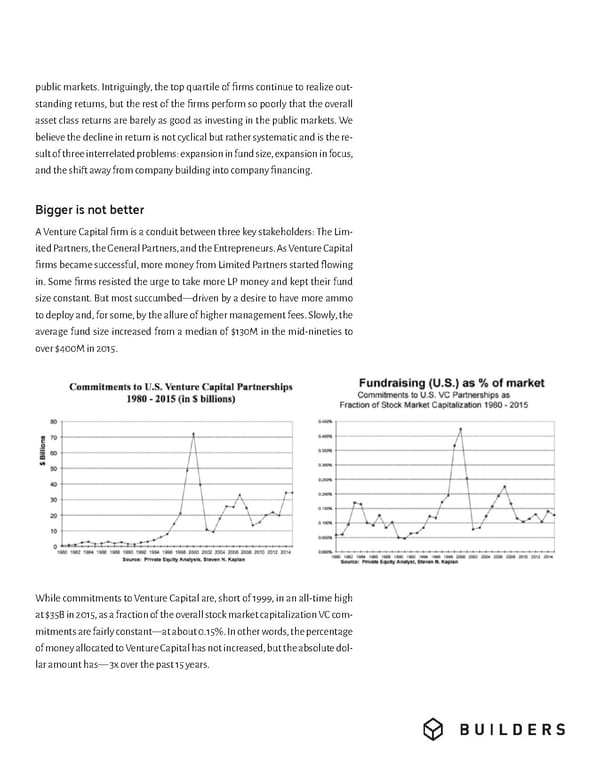

public markets. Intriguingly, the top quartile of firms continue to realize out- standing returns, but the rest of the firms perform so poorly that the overall asset class returns are barely as good as investing in the public markets. We believe the decline in return is not cyclical but rather systematic and is the re- sult of three interrelated problems: expansion in fund size, expansion in focus, and the shift away from company building into company financing. Bigger is not better A Venture Capital firm is a conduit between three key stakeholders: The Lim- ited Partners, the General Partners, and the Entrepreneurs. As Venture Capital firms became successful, more money from Limited Partners started flowing in. Some firms resisted the urge to take more LP money and kept their fund size constant. But most succumbed—driven by a desire to have more ammo to deploy and, for some, by the allure of higher management fees. Slowly, the average fund size increased from a median of $130M in the mid-nineties to over $400M in 2015. While commitments to Venture Capital are, short of 1999, in an all-time high at $35B in 2015, as a fraction of the overall stock market capitalization VC com- mitments are fairly constant—at about 0.15%. In other words, the percentage of money allocated to Venture Capital has not increased, but the absolute dol- lar amount has— 3x over the past 15 years.

Venture Capital - Back To Basics Page 3 Page 5

Venture Capital - Back To Basics Page 3 Page 5